Call or Text (574) 601-3340 to get a cash offer on your house!

Decoding the Financial Implications of a Fast Home Sale

Mar 21, 2024

The decision to sell a home quickly, often driven by the need for immediate cash or the resolution of urgent financial matters, brings with it a spectrum of financial implications. This segment explores the immediate financial impacts of such a sale, including the potential for quick liquidity and the accompanying risks and expenses that sellers should consider.

Immediate Financial Impacts of a Quick Sale

The decision to sell a home quickly, often driven by the need for immediate cash or the resolution of urgent financial matters, brings with it a spectrum of financial implications.

This segment explores the immediate financial impacts of such a sale, including the potential for quick liquidity and the accompanying risks and expenses that sellers should consider.

Quick Cash vs. Potential Losses

One of the most compelling advantages of a fast home sale is the ability to quickly convert a property into liquid assets. This liquidity is particularly crucial in scenarios such as covering unexpected expenses, settling debts, or capitalizing on new investment opportunities.

The speed of the transaction allows homeowners to access funds much faster than the traditional market sale process, which can take months to conclude.

However, the urgency and need for speed come with a significant caveat—potential losses stemming from below-market offers. In their haste to sell, homeowners may find themselves accepting offers that are 10-15% lower than what they might receive in a conventional sale.

This markdown can substantially diminish the financial return from the sale. Prospective sellers must weigh the value of immediate cash against the possibility of losing out on potential earnings from their property.

Cost Savings and Expenses

Opting for a fast home sale also means an end to the recurring financial drain associated with homeownership. Mortgage payments, property taxes, maintenance, and utilities are substantial expenses that cease once the property is sold.

For those in financial straits or facing changes in life circumstances, halting these outflows can provide significant relief and redirect funds to more immediate needs or opportunities.

Despite these savings, sellers must be mindful of hidden costs that can arise during a quick sale process. To make a property more appealing to buyers in a short timeframe, sellers might incur expenses for minor repairs or cosmetic improvements.

Additionally,

fast sales may involve specific fees, especially if sellers employ the services of companies specializing in expedited property transactions. These costs can erode the net proceeds from the sale, affecting the overall financial benefit.

| Benefits | Costs |

|---|---|

| Immediate cash availability | Potential below-market offers |

| Savings on ongoing expenses | Minor repair and staging costs |

| Expedited sale fees |

The decision to pursue a fast home sale is thus a balancing act between the allure of quick liquidity and the potential financial downsides. Sellers must navigate the trade-offs between speed and return, considering both the immediate benefits and the costs that could impact their financial outcome.

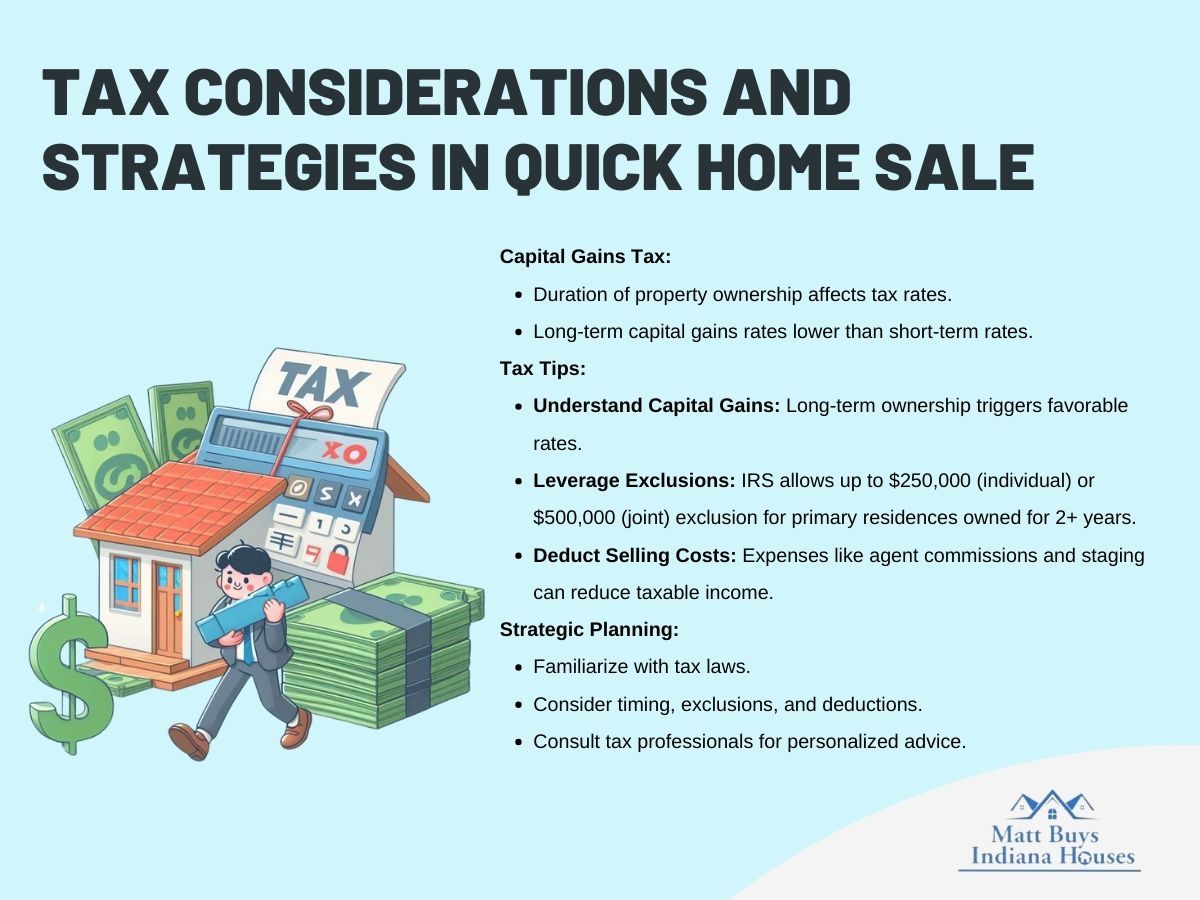

Tax Considerations and Strategies

Navigating the tax landscape is a critical component of selling a home quickly, as the financial implications can significantly affect the seller's net proceeds. Understanding the tax considerations and employing strategic planning can help minimize the tax burden and maximize the financial outcome of the sale.

Capital Gains and Deductions

When a homeowner decides to sell their property swiftly, one of the primary financial considerations is the impact of capital gains tax. This tax is levied on the profit made from selling the property, which is the difference between the selling price and the original purchase price, after adjusting for various expenses and improvements.

The rate at which capital gains tax is applied depends significantly on the duration the property was held before the sale.

Properties owned for over a year before being sold are subject to long-term capital gains tax rates, which are generally lower than short-term capital gains tax rates applied to properties sold within a year of purchase. This distinction underscores the importance of timing in selling decisions, as the duration of ownership can influence the tax implications of the sale.

For many homeowners, the sale of their property can result in a significant financial gain. However, tax laws provide avenues to reduce this taxable income through deductions and exclusions, which can be particularly advantageous in the context of a fast sale.

Key Tax Tips for Fast Home Sellers

- Understand Capital Gains: Grasping the basics of capital gains tax is pivotal. For properties owned for more than a year, the favorable long-term capital gains tax rates come into play. This understanding helps sellers anticipate their tax obligations and plan their sales strategically to benefit from lower tax rates.

- Leverage Exclusions: The IRS offers a generous exclusion on capital gains from the sale of a primary residence. Individuals can exclude up to $250,000 of the profit from their taxable income, while married couples filing jointly can exclude up to $500,000. To qualify, the seller must have used the home as their primary residence for at least two of the five years preceding the sale. This exclusion can dramatically reduce or even eliminate the capital gains tax liability for many homeowners, making it a crucial strategy for those looking to sell quickly.

- Deduct Selling Costs: Another strategy to minimize the tax impact is to deduct selling costs from the sale proceeds. These costs can include real estate agent commissions, legal fees, and expenses incurred for home staging. By reducing the net profit from the sale, these deductions can lower the taxable income, thereby reducing the overall tax liability. It's important for sellers to keep detailed records of all such expenses to substantiate these deductions during tax filing.

Strategic Planning for Tax Efficiency

The tax implications of a fast home sale require careful consideration and strategic planning. Sellers should familiarize themselves with the relevant tax laws and consider how the timing of the sale, the application of exclusions, and the deduction of selling costs can impact their financial outcome.

Consulting with a tax professional can provide personalized advice and help sellers navigate the complexities of tax planning in the context of a quick sale.

By understanding and leveraging the tax considerations associated with selling a home, sellers can make informed decisions that optimize their financial results.

Whether through timing the sale to benefit from long-term capital gains rates, maximizing available exclusions, or deducting eligible selling expenses, strategic tax planning is an essential element of a successful and financially advantageous fast home sale

Professional Fees and Market Timing

When embarking on the journey of selling a home quickly, homeowners are confronted with a myriad of decisions that directly impact the financial outcome of their sale. Two primary considerations in this process are the balancing of professional fees and the timing of the market, both of which play pivotal roles in maximizing returns or minimizing losses.

Navigating Costs

The decision on how to sell your home—whether through a real estate agent, directly to an investor, or via other means—significantly influences the net proceeds from the sale. Engaging a real estate agent typically incurs fees of 5-6% of the sale price, a substantial amount that can reduce the seller's take-home profit.

However, the expertise and market access provided by an agent can often lead to a higher sale price, more than compensating for these fees.

Alternatively, selling 'as is' to an investor might eliminate these agent fees, but this route usually attracts lower offers, as investors factor in the cost of necessary repairs and their profit margin. This option can be appealing for sellers prioritizing speed and convenience over maximizing sale proceeds.

Optimal Timing for Financial Gain

The timing of a home sale is another critical factor influencing financial outcomes. Market conditions fluctuate between sellers' and buyers' markets, largely influenced by supply and demand dynamics.

Selling during a seller's market, characterized by high demand and low inventory, can significantly enhance financial returns, even in a fast sale scenario. Sellers can leverage competition among buyers to secure higher offers and more favorable sale terms.

Conversely, a buyer's market presents more challenges, with a surplus of inventory leading to lower offers and prolonged sale times. In such conditions, sellers may need to adjust their expectations and strategies, possibly accepting lower offers or investing in marketing and home improvements to stand out in the crowded market.

Financing the Next Phase

For sellers looking to transition into another home post-sale, understanding available financial options is crucial. The gap between selling the current home and purchasing the next can present financial challenges, especially in a fast-moving market.

Bridge Loans

Bridge loans are a popular solution, offering short-term financing that bridges the financial gap between selling and buying. These loans allow sellers to use the equity in their current home to finance the purchase of a new one, providing the liquidity needed to make competitive offers.

However, bridge loans come with higher interest rates and fees, reflecting the lender's increased risk. Careful financial planning and advice are essential to navigate this option effectively.

Home Equity Lines of Credit (HELOC)

For homeowners who haven't sold yet but possess substantial equity, a HELOC provides access to funds based on the equity in the home. This can be a flexible option to finance the next home purchase or cover expenses while awaiting the sale. HELOCs typically offer competitive interest rates, making them an attractive option for many sellers.

Renting

Temporarily renting after selling offers flexibility and the opportunity to better understand new market dynamics before purchasing another home. This option can be particularly appealing for those who have sold their home quickly and wish to take their time finding the perfect next property without the pressure of immediate buying.

Long-Term Financial Planning and Reinvestment

The completion of a fast home sale not only concludes a significant chapter in one’s life but also opens the door to numerous financial opportunities.

The liquidity gained from such transactions provides a unique moment for homeowners to reassess their financial landscape and make decisions that can impact their long-term financial well-being and legacy.

Beyond the Sale: Opportunities for Financial Advancement

The immediate aftermath of a home sale is often filled with relief and satisfaction. However, the strategic decisions made with the sale proceeds can define one's financial trajectory for years to come.

Whether the goal is to build wealth, generate income, or secure a financial future, several reinvestment strategies stand out for their potential to meet various financial objectives

| Strategy | Benefits |

|---|---|

| Real Estate Investment | Potential for passive income |

| Stock Market | Diversification and growth |

| Retirement Accounts | Tax advantages and compound growth |

Reinvesting in Real Estate

Investing the proceeds into real estate can offer a tangible and potentially lucrative avenue for wealth generation.

Whether through purchasing rental properties for passive income or investing in real estate investment trusts (REITs) for easier entry into the market, real estate continues to be a favored option for many investors. This approach can provide not only a steady income stream but also the potential for capital appreciation over time.

Diversifying into Stocks and Bonds

For those looking to diversify their investment portfolio, allocating a portion of the sale proceeds into the stock market can offer substantial growth opportunities. Investing in a mix of stocks, bonds, and other securities can help manage risk while striving for higher returns.

This strategy benefits from the potential for capital growth and income through dividends, alongside the flexibility to adjust the portfolio according to changing financial goals and market conditions.

Contributing to Retirement Accounts

Maximizing contributions to retirement accounts such as IRAs or 401(k)s with the sale proceeds can offer significant tax advantages and the potential for compound growth. This strategy is particularly effective for securing long-term financial stability, providing a foundation for a comfortable retirement.

The tax-deferred or tax-free growth (depending on the account type) allows investors to maximize the impact of their investment, underscoring the importance of retirement planning in overall financial health

Integrating Sale Proceeds into Broader Financial Planning

The integration of sale proceeds into one’s overall financial plan requires a holistic approach, considering factors such as estate planning, tax implications, and long-term financial goals. This integration ensures that the decisions made post-sale align with the individual’s or family’s broader financial objectives, from wealth preservation to legacy building.

Estate planning, for example, can be an essential consideration for those looking to pass on their wealth to the next generation. Decisions made with the sale proceeds can significantly impact estate taxes and inheritance plans, making it crucial to consider these aspects when reallocating funds.

Similarly, understanding the tax implications of different investment options can help maximize the efficiency of reinvestment strategies. Consulting with financial and tax advisors can provide valuable insights into how best to utilize the sale proceeds in alignment with one’s financial landscape and objectives.

FAQs

What are the main financial benefits of selling my home quickly?

The primary financial benefit is the ability to quickly convert your property into liquid assets, which can be crucial for covering urgent expenses or seizing new investment opportunities. Additionally, you'll save on ongoing costs related to homeownership, such as mortgage payments, property taxes, maintenance, and utilities.

What are the potential financial downsides to a fast home sale?

The most significant downside is the potential for accepting below-market offers, which could be 10-15% lower than what you might achieve in a conventional sale. Additionally, there may be hidden costs, such as minor repair or staging expenses and specific fees if you're working with companies that specialize in quick sales.

How can I minimize the tax impact of selling my home quickly?

Key strategies include understanding and planning for capital gains tax, leveraging exclusions (up to $250,000 for individuals and $500,000 for married couples filing jointly if the home was your primary residence for at least two of the five years preceding the sale), and deducting selling costs like real estate agent commissions and legal fees.